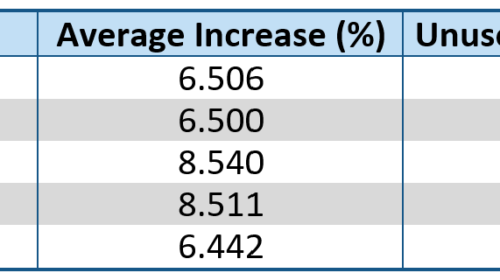

In the latest example of how Postmaster General Louis DeJoy defines “prudent and judicious,” he won Board of Governors support to seek the second price increase on market-dominant products in less than a year. As in the prior rate hike, effective last August 29, DeJoy opted to use nearly all available rate authority. If approved by the Postal Regulatory Commission,…

Read MoreUSPS Files for Second Market-Dominant Price Increase in a Year